According to Gründerszene, the Berlin-based solarisBank might raise a Series B. Whether this will indeed happen does not matter (the news is actually from October). What matters, however, is solarisBank’s position in the FinTech value chain. solarisBank is a banking platform which owns a banking license and offers financial services such as bank account management, credit card issuing or KYC (know your customer) services. In short, the bottom of the stack, the infrastructure of FinTech companies — as some would say — the boring stuff. In contrast, N26 and revolut are doing the exciting, customer-facing stuff; offering an easy to use, nice looking banking app.

From a strategic perspective, however, the „boring“ stuff, is actually the sexy stuff (if banking can be sexy at all). This is not only because solarisBank per se is attractive (in many cases they are the backbone of FinTechs), but also because N26 and revolut are playing in an extremely difficult market.

Slow customer acquisition and market saturation

Whereas there are several difficult things about banking, the one I am referring to is customer acquisition. For instance, Scalable Capital, a robo advisor partnering with ING-DiBa, shows how difficult customer acquisition can be and, in turn, the power of having a customer base. Recently Scalable Capital announced that around 1/3 of their €500 Million in assets came through partnering with ING-DiBa for two months (press release).

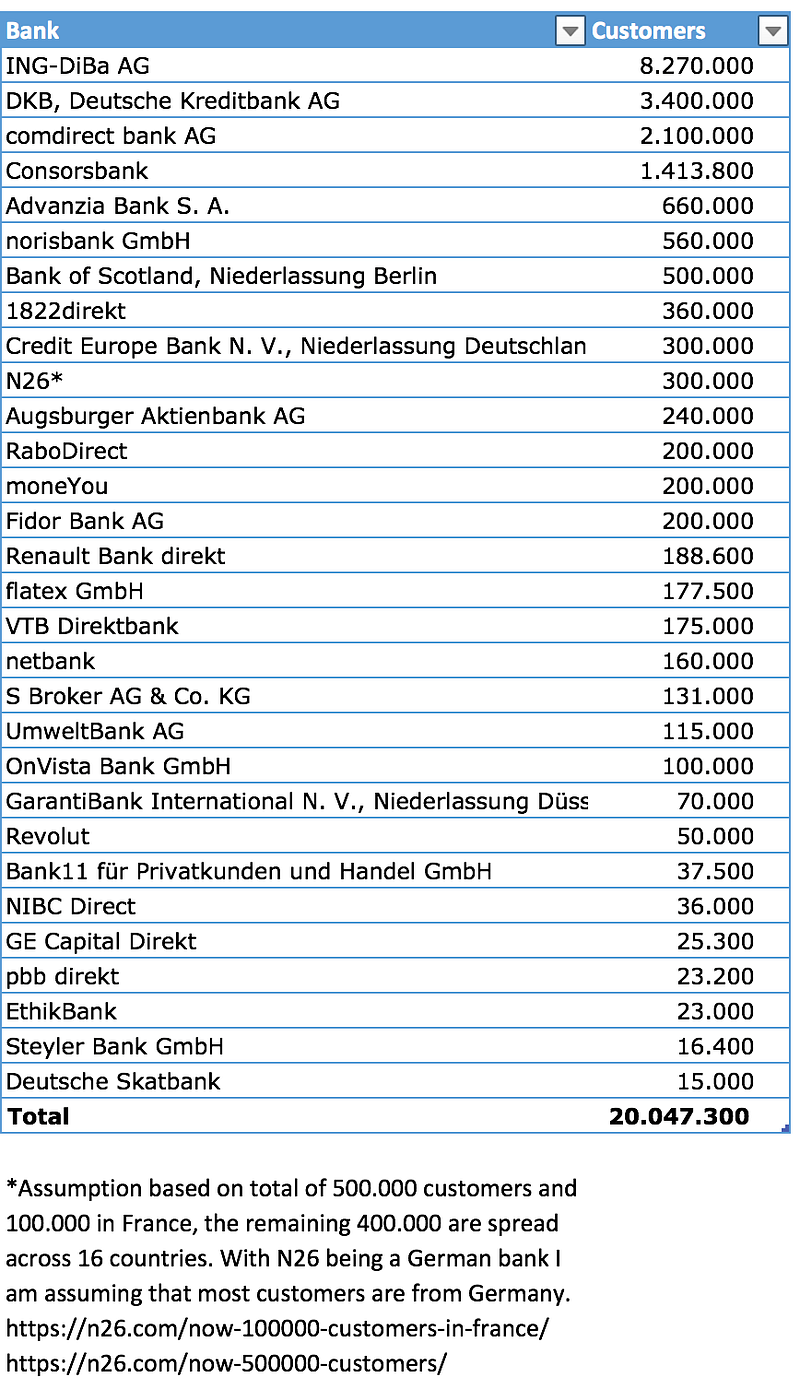

Consider in this context how Germany’s three biggest direct banks (ING-DiBa AG, DKB, and comdirect bank) have around 14 Million customers (out of the 20 Million total direct bank customers).

This is significant for a couple of reasons.

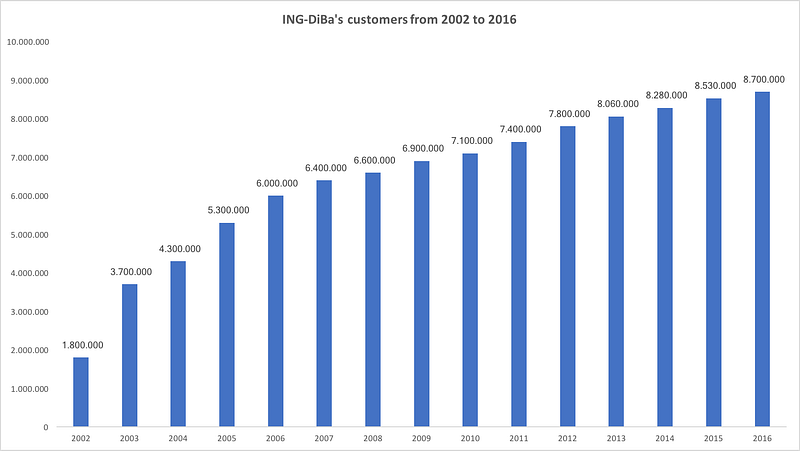

Firstly, it took them long. I would say around ten years. Although ING-DiBa, for instance, has been operating for more than ten years, as smartphones — what revolut and Co. depend on — only exist since the iPhone’s debut in 2007 (smartphones have been around longer but it wasn’t before the iPhone that they became relevant) 2007 is a more realistic starting point.

Secondly, everybody below the age of 18 already has at least one banking account when you couple the 20 Million direct customers with the 40 million customers of all Germany’s bank branches and a bankable population of around 50 Million.

Furthermore, the market is difficult because incumbents are “fairly” good.

Incumbents are rich and have — despite slow product development — fairly good “FinTech products”

Both, N26 and revolut are well funded and grow in manpower. N26 €45 Million in funding and 250 employees (on LinkedIn), revolut 209 employees (on LinkedIn) and €73 Million funding. However, comdirect and ING-DiBa have significantly more. ING-DiBa has €7.7 Billion in equity and 3.938 employees, comdirect around €600 Million in equity and 1.444 employees (based on annual letters; comdirect and ING-DiBa’s German annual letter).

Looking just at ING-DiBa’s hard facts and their “FinTech products” in relation to N26 reveals two things. On the one side, it shows that their product development is slow relative to their cash reserves and manpower. On the other side, however, it shows that their offering is less and worse, but still good enough.

ING-DiBa’s fairly good “FinTech products”

With N26’s app you can

- Do the basic banking stuff: check your balance and make transactions

- Save money (through WeltSparen)

- Invest (through vaamo)

- Take up a loan (through auxmoney or N26)

- Manage your insurances (through Clark)

- Transfer money abroad through TransferWise

ING-DiBa offers four apps (app names in bold):

- Banking to go: for making transactions

- Kontostand App: only for checking your balance (with a multi-banking feature). I think it is weird that you have a dedicated app just for checking your balance. And apparently so does ING-DiBa; they announced that multi-banking will be integrated into the Banking to go app.

- Banking + Brokerage: combines Banking to go with security trading. Security trading is another feature that they will integrate into the Banking to go app (not sure what the difference will be)

- ImmoWert2Go: gives you approximate values of houses or flats you photograph. Whereas I believe that convergence among industries makes sense (here FinTech and PropTech) and ImmoWert2Go is a cool app, it looks totally misplaced along payment and banking apps (or not, but more why later).

- paydirekt: a payment app (not theirs, but they advertise it on the website) nobody uses paydirekt and paydirekt has some serious struggles.

However, although ING-DiBa has a worse user experience and offers less, they still have more customers, and their customer base has been growing ever since.

With that in mind, one could argue that these „challenger“ banks shouldn’t even try competing with incumbents because they stand no chance. To some extent that is what, for instance, ING-DiBa and comdirect believe. Both have argued in their 2016 annual letters that they do not see FinTechs as competitors but rather as an opportunity for cooperation. And as so often, history repeats itself. Similar words were issued by Blockbuster and Nokia who then were put out of business by Netflix and Apple, respectively. However, there are a few essential differences between „then“ and „now“ which favor incumbents.

Incumbents are aware of FinTechs and profit similarly to startups from a technically favorable environment

Firstly, incumbents are aware that things are changing. comdirect, for instance, collaborates with startups through their startup garage and pushes entrepreneurial thinking through their Entrepreneur in Residence program. ING-DiBa, for instance, is one of the leading partners of Frankfurt’s TechQuartier, a hub for startups, corporates and similar. Among these startups are some well-known FinTechs such as vaamo or easyfolio. Also, as shown above with ING-DiBa (comdirect also has a nice array of apps and services), incumbents are — although slowly — “digitalizing” (at least on the front-end). Furthermore, if „boring“ FinTechs such as solarisBank make life easier for startups, they can do for incumbents as well.

(Please note that ING-DiBa and comdirect are not representative of all direct banks. I have only used them to demonstrate that there are some really serious incumbents in the banking market.The situation might look completely different with some of the smaller ones.)

Anyway, whereas it would be risky to ignore incumbents’ cash, manpower and customer base, there are still a couple of interesting angles for startup banks.

Trigger-events as customer acquisition strategy

The first interesting point relates to customer acquisition. In regards to volders, a Berlin-based contract management startups, I argued that the dependency on trigger-events makes customer acquisition difficult for them. I believe it is even worse for banking. If you are a bank customer, you won’t wake up one day and say “I need a new bank. Let’s go get me one.” (If yes, let me know, sounds like an interesting thing to do) Rather, you would switch when something — a trigger — occurs. The disappearing of branch banks and growing consumer awareness are two such triggers.

Disappearing bank branches and growing consumer awareness as trigger-events

Although branch bank and direct banks serve different customers, branches will disappear and I believe that there will be dissatisfied customers who, once forced to used branch banks’ very rudimentary apps, (for instance, the Sparkassen app — Sparkasse has around 40 Million customers — offers a similar feature set as ING-DiBa) will switch to direct banks. Whereas direct bank customers are used to having a limited offering, branch bank customers who can get all kinds of services from their local store, are not.

Furthermore, although other industries are driving consumer preferences in banking, people might simply be unaware of “modern banking” due to the low publicity of newcomer banks. Nevertheless, people’s preferences will eventually shift, and they will go looking for a new bank (here the trigger event is the preference shift). Once that happens, the question is — as Alex Rampell from Andreessen Horowitz puts it — whether the startup gets distribution before the incumbent gets innovation. Unfortunately, I haven’t yet spent enough time with incumbents, but I think that especially small banks (based on customer size) won’t get innovation quickly enough. Whether these direct banks will be startups or incumbents is to be seen, but N26 — who has a hybrid version between direct and branch banking (for instance, you can deposit money at certain supermarkets) — is in a very interesting position. N26 is furthermore in a very interesting position because their full stack offering allows for a range of trigger events.

N26’s full stack offering allows for multiple trigger events

N26’s offering (banking, having a credit card, saving, investing, taking a loan, managing insurances and transferring money abroad) coupled with their eight-minute sign-up process, allows for a range of trigger events. When you need a loan, credit card, want to save money etc. you might end up on N26’s website and because creating a bank account takes only eight minutes, you might as well open one although you initially came for something else.

N26’s full stack offering is also interesting from a pure product perspective as it points at the opposite direction of where most FinTechs are heading.

Re-unbundling in FinTech

Generally, an unbundling can be observed amongst FinTech startups; they pick a certain bank offering — like investing — and create a better, standalone product based on it.

N26 and revolut do the opposite. They take these verticals and re-unbundle them again into one app. This re-unbundling merits to question whether it makes sense to bet on a bank app as the banking app of the future and if yes, how much should such an app offer.

Banking apps or verticals as the customer interface

Consider how easy it is to be a “bank”. Outbank, an app for multi-banking (who recently got acquired by Verivox; German press release) could be a great solution for the one quarter of all Germans who have three or more bank accounts. By using Outbank (or any other multi-banking app for that matter) for managing their finances and one of the dedicated apps and providers for everything else, people would be banking without using their core banking app.

Moving forward, I believe it is legitimate to ask whether your bank’s banking app, will be as central for banking-related activities — checking your balance, making transactions — as they are now or whether they will move all the way down in the stack and just be the infrastructure provider. For instance, I have argued here that merging insurances into finance makes a lot of sense but revised my statement when I looked at ottonova and Ada health. Such an increased importance of insurance might devalue the importance of, for instance, N26 and revolut who integrate insurance into their offerings.

Assuming, however, that your core bank’s app will be your focal banking interface, leads to asking the “value chain depth” question.

Banking apps’ value chain depth

With the “value chain depth” question I refer to the number offerings that will be re-unbundled into the traditional banking app. Will it be a re-unbundling into banking apps that offer as much as HSBC from the picture above or will ING-DiBa’s depth be the way forward alongside an emergence of specialized verticals (e. g. one app for saving, one for transferring money between friends, one for investing…) or are N26 and Co., who bundle a few services, the “sweet spot”? Or, will the “banking app of the future” move beyond money-related topics (maybe ING-DiBa’s ImmoWert2Go is not so misplaced after all)?

Notes

[1] *Assumption based on a total of 500.000 customers and 100.000 in France, the remaining 400.000 are spread across 16 countries. With N26 being a German bank I am assuming that most customers are from Germany.

Disclaimer: I am an N26 customer. No endorsement, however.

As a side note, Verivox recently also acquired Aboalarm — a company for contract cancellation (German press release). Also, Outbank temporarily filed for bankruptcy (German press release) and Zuper, a similar startup based in Germany, is expanding to Austria (German press release).

Update: Changed “Scalable Invest” to “Scalable Capital”. Thanks to Lasse Groth (LinkedIn) for pointing out!