The German mobile bank N26 announced that they are expanding into the USA. This announcement comes almost exactly one month after revolut, their biggest competitor, launched its operations in Austria and Germany (I wrote about revolut in revolut, N26, and the future of banking). Also, this announcement comes only a few days after revolut’s announcement of the cooperation with the InsurTech startup simplesurance.

simplesurance — a test case for simplesurance and the industry

This partnership is interesting due to several reasons. Specifically, in regards to simplesurance, it is interesting because their simplesurance’s solution for revolut does not stem from their standard offering. simplesurance, the Berlin-based FinTech, has three offerings: B2C products such as simplesurance.co.uk through which they offer insurance for consumer electronics, insurance cross-selling for e-commerce, and an insurance broker.

I guess that this is a test case for them and — if successful — going to integrate that as a standard offering. As it is concept-wise similar to their cross-selling solution, it makes sense to incorporate that into their offering from a portfolio perspective. From an industry-perspective — and this is another interesting aspect of this cooperation — it makes sense as well because it points at the convergence of InsurTechs and other industries.

Convergence between InsurTech and other industries

Insurtech is becoming integrated into a range of different industries. The cooperation between revolut and simplesurance is convergence in two very related fields, insurance, and finance. However, we see that also in more distant industries. The most extreme example is PayKey. PayKay, who recently raised $10 Million, is a banking smartphone keyboard. Users can access banking services like transmitting money or balance checking directly in the keyboard. The idea is to remove friction by allowing customers to access banking services from wherever they are. Whether users want to bank from anywhere, I doubt, but this discussion would miss the overall point, which is the seamless integration of finance and banking into consumers’ lives.

Furthermore, we see industry convergence in product-wise different fields. For instance, health care and insurance. Whereas those two industries are linked by design in Germany (your insurance pays for your medical expenses), your still have to interact with two institutions. ottonova, however, who combines insurance and health care, and thus offers both products one. Another company in that regard is BuddyGuard, the Berlin-based smart home startup whose recent funding I covered in BuddyGuard & Chatterbug: Storytelling, smart home network effects and the future of edtech. BuddyGuard’s security camera FLARE can be enhanced by add-ons that automatically contact the police and a live-stream to BuddyGuard’s monitoring center in case of an emergency. In the post above and also Parce, Pariot and home-ix (three German smart home startups) I have argued that a smart home derives most of its value through network effects (the more smart home devices you own, the more value your home has to you. In fact, it might be of value only after it reaches a threshold of a certain amount of smart devices). Looking at BuddyGuard but especially at Neos (The UK-based startup, backed by, amongst others, the German-based InsurTech VC InsurTech.vc. combines smart homes — through security products — and home insurance), I think that the combination of services — especially insurance — into smart homes could be a value proposition for smart homes as important as network effects.

What this combination undoubtedly, however, implies, is the tight integration of insurance into products. Take as another example Daimler’s pay-as-you-drive car insurance which is directly integrated into the car through sensors.

This changes the way people approach insurance. Instead of buying a product and visiting an insurance company, these examples imply that in the future we will buy a product with integrated insurance. This is interesting because it removes one of the biggest hurdles startups have, namely access to consumers. If they partner with product companies, they instantly get access to consumers. This, however, also pushes insurers upwards in the value chain out of distribution into supply. The consequence of this shift is their disappearance in consumer’s mind. getsafe provides another form of industry convergence.

getsafe and the power of a customer base

Back in September, getsafe, a German FinTech start-up announced that they are turning themselves into an insurer. Without a BaFin-license but through a cooperation with Munich Re and Munich Re’s subsidy Digital Partners, they are going to position themselves as a multiline insurer. Through this multiline portfolio, they will offer property & casualty (P&C), health and life insurance „in the coming months“. Before that shift, getsafe was a mobile insurance wallet. This service is still available under the name: Der Versicherungsmanager — powered by GetSafe.

As the reason behind their foray into insurance getsafe mentioned the knowledge, they gained about the insurance industry through their insurance wallet customers. However, I think what drove them more was their customer base of 20.000 users. Relative to the about 500 (!) insurers in Germany and their customer bases (HanseMerkur, not even the biggest insurer, had almost 8 Million customers in 2014), getsafe’s customer base is insignificant, but compared to COYA or ONE (see below) who operate in a similar field, are not yet available, and thus have zero customers, 20.000 does not sound that small. As their products are not yet available, not much can be said except the following. Firstly, as already indicated, they are fighting a very difficult battle because of incumbents. Secondly, with their multiline approach their competing directly with these incumbents. There are several other startups that pick one or more (niche) insurance products and spin them out into standalone products. The most popular are electronics insurances such as the mentioned simplesurance, but we can also see that with cars (Metromile, for instance, offers pay-as-you-drive car insurance) or Haftpflicht Helden for Liability insurance. Although acquiring customers (or up-selling them in getsafe’s regards) is difficult in the insurance industry, people will switch if the product is significantly better than alternatives. getsafe has three ways to be significantly better than their competitors.

- Differentiate because their multiline serves customers as a better one-point solution than incumbents

- Make each type of insurance better than their competitors’

- Combining 1. and 2.

I believe that the most effective way would be to either create a great one-point insurance solution (option 2) or pick a certain type of insurances and deliver them in a way incumbents are not. Going back to the above-mentioned ottonova, I think that they are a good role model of how you can pick a product within a crowded market and offer something significantly better. Currently, it seems that getsafe takes a traditional insurance company and improves the UX (easy sign-ups, claim management…). I doubt that this will be enough for a market as crowded as the insurance industry.

volders and the power of a customer base

In this context, I want to update my thoughts on volders, a Berlin-based contract management startup that raised two million euros in September. volders is a personal contract assistant. You feed the application with your contracts, and it manages them for you. You are alerted about contract expiration, you can cancel or prolong contracts, and in combination with a built-in price comparison tool you can compare and sign up for new contracts. I wrote about their investment here and was very critical of their product;

Contract management is trigger-based (you switch your contract only through a trigger in your life) and the diminishing value of contract optimization (you can cancel or get a better offer only a limited amount of times). Besides that, volders is in a difficult business because there is a limited amount of contracts (certain contracts you would never cancel), people have little motivation due to delayed rewards and uncertainty, customers’ avoidance of dealing with contracts and though competition.

There is more one thing that might make their life a little bit harder. Germany’s cartel office announced that they would be looking into the recommendation practices of online comparison portals because they have doubts about their objectivity and customer-orientation. volders has a comparison platform built-in and might be inspected by the cartel office as well, but in general, I doubt that this will have big effects on neither volders nor any other company in that sector.

Leaving these problems aside, I made a huge mistake in my volders analysis. Although I mentioned their customer base of 550.00 users, I overlooked their potential in regards to a strategic move similar to the one volders did. In regards to contract management 500.000 users is a niche, but in regards to getsafe, revolut (who has around 800.000 customers), Coya and ONE (see below), all but a niche. Whether volders will indeed move into the insurance industry is unclear, but at least they have the customer based. I strongly believe that they will.

All that just mentioned except getsafe and volders (insurance disappearing in the value chain and the convergence between InsurTech and other industries) stands in sharp contrast to Coya and ONE.

Coya and ONE and emotional positioning of insurance

Berlin-based InsurTech COYA is a fully digital insurance which has raised $10 Million in August, among others, by Peter Thiel. There is not yet much to say about Coya except that they present their insurance in a very emotional way, almost as a lifestyle product. Their catchphrase: “BE BOLD. We’ve got your back.” Their mission statement:

Insurance could be so much more…

Insurance was born to protect peoples interests, a wonderful cause! But the insurance empire is broken and it’s time to strike back at its legacy infrastructure, organizational design and products built for broker intermediaries rather than around customer. Coya offers a new hope, by redesigning and extending the insurance value chain, working backwards from the customers real life needs. Coya will offer scalable protection at the point of need with an AI risk guardian and simple, transparent and personalized insurance cover. Designed from the ground up to manage life’s risks and join our customer’s journey.

Smile. We got your back.

ONE, also fully digital insurance, which is about to launch their offering this fall, has a similarly emotional messaging, but focuses intensively on “customer first”. Their website and product video represent that fairly well (unfortunately I cannot embed the video here, but you can watch it on their website).

This is emotional positioning is interesting for two reasons. Firstly, it something established insurance companies do not have and secondly, it merits to discuss the power play between FinTech (as represented by banking startups such as N26 or revolut) and InsurTech (as represented by insurance startups such as Coya).

revolut’s and N26’s foray into insurance (N26 integrates insurance contract management into their app by partnering with Clark) shows that they — one of the biggest full digital banks — want to control the the Insurance-Finance stack and push insurance startups up in the value chain and turn them into suppliers.

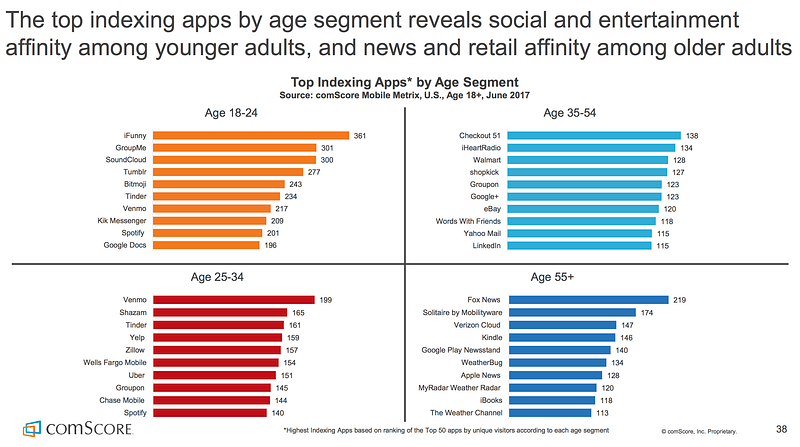

ONE, Coya, and getsafe, however, take the view that — metaphorically speaking — standalone insurance apps merit more user attention. Sticking with the app-metaphor, it merits to look at the top indexing apps according to comScore’:

Venmo is #7 among 18–24 years-olds and #1 among 25–34 years old. Also in the 25–34 age group, two dedicated banking apps, Wells Fargo Mobile and Chase Mobile Banking take place #6 and #9, respectively. If we stick with the first two age groups, we can see that FinTech apps play a certain role in users’ everyday lives. That is, of course, data picking because, for instance, finance does not play a role at all among “top apps” or age 35–54 and age 55+.

One could further argue that no insurance apps are listed because there are less available of those, but a certain presence of finance apps can be explained by their very nature (you need them multiple times a day for several reasons). By that logic then, insurance companies should not invest too much time into developing standalone apps because there is simply no inherent need. Usually, you are in touch with your insurance for three things; sign-up, processing claims and canceling. All that, however, can be integrated into other services as revolut or volders, for instance, show. Thus, no standalone insurance product needed. This is, of course, an exaggeration, but I think an important one that should point at the general question of whether a new FinTech is really a new product or just a better UI/UX and whether we are working on something just for the sake of technology or because we see an essential problem that needs solving.