paydirekt might get €300 Million from its founders. It is estimated that paydirekt has already received €100 Million. At the same time, paydirekt’s CEO, Niklas Bartelt, should be replaced (from Süddeutsche).

paydirekt was founded by a couple of German banks in 2015 and offers C2C and online B2C payments. Martin Zielke, board chairman of Commerzbank, argued back in 2015 that paydirekt was not founded with the idea of replacing the competition, but rather co-existing with them as — so Zielke — the online payment space has room for more than one company (from Süddeutsche). I agree with Zielke, but it is also a very undifferentiated market where people won’t switch unless given a very good reason.

The most significant reason in C2B is network size, i. e. how many shops support the system. This significance of network size implies the vital role of pull marketing; there is little use in convincing people to sign-up for a new service now, so that they can use it later. Instead, people will access an online shop, realize that there is a payment solution they do not have – but need – and thus sign-up for that very service.

paydirekt’s push marketing questionable

This pull scenario — the user realizing that there is a payment service she needs but does not have— is extremely rare in Germany. PayPal, paydirekt’s biggest competitor, is available at 50.000 shops, paydirekt at 1500 [1]. Furthermore, only a fraction of these 1500 shops — around 50 — are among the top 1000 e-commerce shops. Besides this market structure that makes the coincidental appearance of a pull scenario unlikely, the Sparkassen — one of the biggest bank group behind paydirekt — are actively pursuing a push strategy. In August they announced that they will be pre-registering bank customers for paydirekt. This means that each of their bank customers will be automatically registered at paydirekt unless they explicitly opt-out. Whether this is actually legally allowed is currently under discussion, but it clearly shows paydirekt’s aggressive push strategy. Compare that to PayPal’s customer acquisition in its early days where each user received money for signing-up and recruiting others. PayPal’s strategy was, of course, far more expensive in the short-term, but in the long-term, it helped them increase PayPal’s network power exponentially. For a user, each additional user increased the network’s value as she had one more user to send money to. For merchants, each PayPal user increased the incentive to adopt PayPal.

Although PayPal’s cash reserves were limited back then, they survived their growth hacking. In this regard, paydirekt is different. They have deeper pockets but seem to be spending the money on the wrong ends. For instance, they paid the e-commerce company Otto several million (t3n reports 13 Million, Handelsblatt a high seven digits figure) to become integrated into their online shop otto.com.

Three-sided network slows customer acquisition

However, not only shows this investment into Otto paydirekt’s push-marketing approach, it also shows one reason for their slow expansion, namely their network infrastructure. Whereas PayPal is a two-sided market (users and merchants), paydirekt has three sides; users, merchants, and banks.

Lower learning curve, lower scale economies and inter-bank competition due to three-sided market

With paydirekt pre-registering customers, I have touched upon one problem in this constellation. To use paydirekt, you must have an account at one of the participating banks. This means that each bank must acquire customers on their own. This leads to a lower learning curve, and lower scale economies than centralized competitors like PayPal have. Also, as people tend to have multiple bank accounts at the same time, banks compete against each other for customers as the banks only profit from their customers. The situation is the same for merchants but with a few additional caveats.

Slow customer on-boarding and missing transparency due to three-sided market

The most prominent caveat in this bank-merchant relationship is that the manual process. If a shop wants to integrate paydirekt, they must talk to banks before they can start accepting payments through paydirekt. Compared to the fully digital online process at PayPal, which takes around two minutes, paydirekt’s approach is more than questionable, especially for shops who are just getting started and hardly have the resources for their core activities.

Also, whereas paydirekt is free for end users, merchants get different conditions from different banks. Whether this will lead to merchants shopping around is unlikely (they would need multiple bank accounts for that), but it is the opposite of transparency and could lead to frustrated merchants who realize that another bank charges a competitor less for the same service.

paydirekt’s biggest advantage — customer base — rendered obsolete due to a non-existing value proposition

In this context, it merits to highlight hat paydirekt actually already has the network of merchants and consumers, namely through their existing customers. In simplesurance, getsafe, Coya, and ONE — convergence, emotions, and power of customer base in FinTech I pointed at the fact that a customer base is crucial in the insurance industry. The same is true for the payment segment, but as the digital banks N26 and revolut have shown (see revolut, N26, and the future of banking), if something better than the existing solution comes up (and people are aware of it), users will switch. PayPal’s offerings show that paydirekt has — as the saying goes — been playing where the puck is instead of where it is going to be, thus not being better than existing solutions and rendering one of its biggest advantage — customer base — obsolete.

PayPal’s offering in Germany is as follows:

PayPal’s B2C offering

- Shop online via PayPal (including discounts for PayPal-customers)

- Send money nationally and internationally

- Request money from other people

PayPal’s B2B offering

- Use PayPal to accept payments or donations

- PayPal Plus: Use PayPal as a payment solution (allows shops to provide paying through debit, credit card and bill to end consumers)

- Deferred payments

- UX-based products: PayPal Express Checkout, e-mail-invoicing, selling on eBay, mobile selling

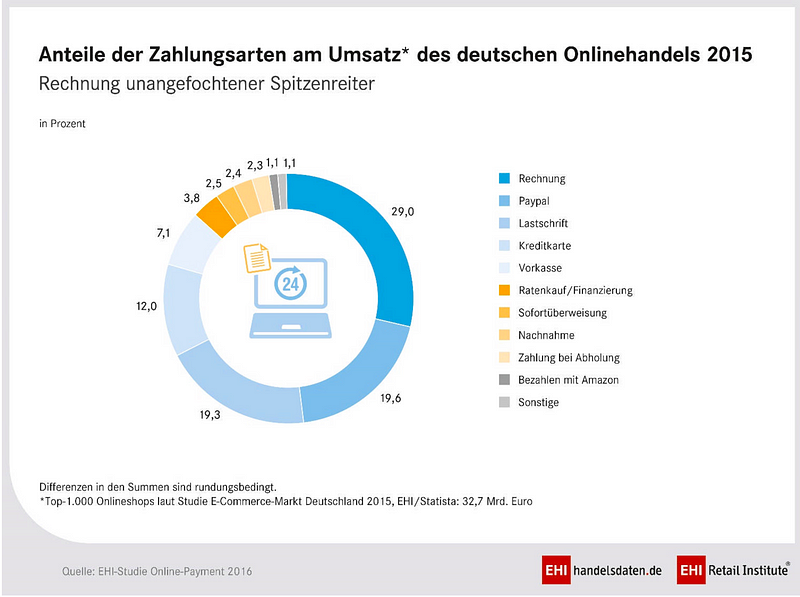

PayPal Plus is especially impressive when you consider that in Germany around 20% of the whole e-commerce revenue flows through PayPal, 29% through bills, approximately 20% through debit, and 12% through credit card. It is no coincidence that all payment methods covered by PayPal Plus equal around 80% of the revenue. As a consequence, PayPal’s market share is probably above 20%.

Furthermore, this implies that Germans apparently still prefer traditional payment methods (bills, debit…) over digital alternatives such as PayPal or paydirekt.

POS payments a chance for paydirekt

With all that in mind, one can see that paydirekt’s battle for customers and merchants is tough (this does not even include new competitors with massive customer bases such as Apple Pay which will come to Germany eventually). This does not mean, however, that paydirekt has no chance in that field, especially with the massive customer base. This does, however, mean, that paydirekt must solve the here mentioned fundamental problems and — to re-use the metaphor — go where the puck is going. One area where the puck is going in Germany is Point-of-Service (POS) payment. PayPal and Apple already offer that outside Germany, but here the market is still very fragmented. Based on what paydirekt has done until now, I fear that they won’t embrace that field, or only after Apple or PayPal have done so, but they definitely should. If they don’t, we will have a discussion similar to this one in a few months, just centering around POS payments instead of online.

€500.000 for happybrush

happybrush pitched their electric toothbrush at this week’s Die Höhle Der Löwen (DHDL). They wanted 10% for 500.000€ but went home with 500.000€ for 20% by the two investors Ralf Dümmel and Carsten Maschmeyer.

According to the founders, their toothbrush is special due to a pressure sensitive and very effective cleaning head, a three-week lasting battery, a charging station with a built-in countdown, their aesthetic design, environmental friendliness, and a „fair price“.

One reason why I looked into happybrush was to understand why Ralf Dümmel and Carsten Maschmeyer – both experienced investors and entrepreneurs – invested, because to me it was no investment case. I know why they invested, but do not understand it. They invested because they can offer shelf space to happybrush and because they believe in the potential of the smart connection to insurance (see below).

Plans are too long-term and only slightly better product

However, smart toothbrushes, in general, are a very distant future. Furthermore, shelf space is important, but people will not buy happybrush if a better product is right next to it.

Smart toothbrushes are very far in the future

One of the things happybrush provides is „Oral car that really cares“. They do that through a smart toothbrush add-on. One of that adapter’s features is the integration of insurance into the brushing process. This should lower insurance premiums based on cleaning behavior.

I am unsure whether brushing-based insurance premiums will ever be part of our everyday lives because it is such an insignificant improvement. Besides that, however, a lot of other things are possible in the context of „brushing and data“. One example is home diagnostics. I am a big fan of home diagnostics and In Cara, a German PoopTech-startup, received a $2 Million investment for a food diary and tailor-made drugs I argued that such a decentralized approach to medicine makes a lot of sense as it could lead to custom-made treatments and doctor-free diagnosis. In regards to toothbrushes, technology could track our teeth’s and mouth’s condition (caries, misaligned teeth, etc.). But, a long, long time will pass before such things become a reality. (It might even take so long that another technology makes teeth cleaning redundant in the first place.)

happybrush neither better nor cheaper

happybrush offers nothing that makes them significantly better than incumbents. Slightly better cleaning, longer lasting battery, and similar features are only very marginal improvements.

In regards to price, happybrush claimed that their heads are 1/3 of their competitors’ prices. However, something does not add up as happybrush’s heads cost around 3€/piece and Oral-B’s range from 2€ to 4€. Also, Oral-B offers a range of brushes and heads below happybrush’s prices.

Nevertheless, there are three additional interesting themes around happybrush.

Value chain

From a value chain perspective, they are similar to the Munich-based car startup Sono Motors. Similar to Sono Motors, they neither produce nor design their products (Sono Motors, however, designs their car).

With Sono Motors I criticized that they are outsourcing — what should be their core competency — car manufacturing;

“In the long-term the company will benefit from starting producing as early as possible. Economies of scale, learning and experience curves (lack of R&D and engineering) are the most fundamental reasons for that. By not having direct access to the core of their product I have troubles believing that they will be able to defend them successfully against competitors and suppliers in the long-run (think of the knowledge suppliers are accumulating, eventually sharing with other companies or even integrating forward). Furthermore, they are outsourcing one of the things that make them unique sustainability (batteries and solar panels).”

I think I must change my opinion on that. In fact, it might indeed make more sense to focus first on validating your idea by outsourcing its creation instead of spending too much time on the core things, especially as these core things are activities your competition is extremely good at. For Sono Motors the extremely good competition are OEMs and for happybrush, this is, among others, Oral-B.

Convergence with FinTechs and foray into smart homes

In Parce, Pariot, and home-iX (three German smart home startups) I wrote that network effects will be the main value driver in smart homes, but I extended on that in simplesurance, getsafe, Coya, and ONE — convergence, emotions, and power of customer base in FinTech by adding that the integration of services — especially insurance — into smart homes could be a value proposition for smart homes as important as network effects. In that same article, I also pointed at the product-wise convergence in the the FinTech market where insurance becomes integrated into products. With happybrush we see both of that happening; they are bringing services to the smart home and integrating insurance with hardware.

Business Model Innovation

When looking at happybrush’s revenue driver, the heads, I wondered whether a subscription model would fit them. I went on to compare them to the Dollar Shave Club. Dollar Shave Club (DSC), selling razor blades through a subscription model was acquired by Unilever for $1 Billion in 2016. Their success originates in them disrupting (by definition) the blades and razors market.

At the time they started their operations the blades and razors market looked (and still does) as follows:

- Dominated by a few big companies

- selling over-engineered products (multiple blades, battery-powered razors…)

- at a premium price

- to consumers indirectly through retailers

- advertising their “neutral brand” on everything except social media but with big media budgets.

DSC approached that market differently.

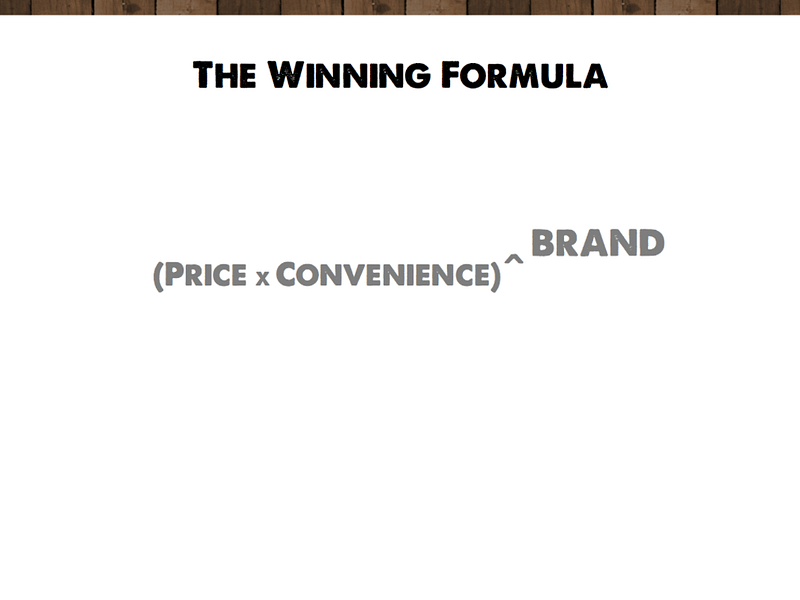

Their strategy is summarized in their winning formula:

They offered simple products (two blades) at a low price (1$ monthly), selling directly to consumers and marketed through social media focusing on lifestyle (see their video below).

There are a few similarities to happybrush’s market:

- Dominated by a few big companies selling

- to consumers indirectly through retailers

- advertising their “neutral brand” on everything except social media but with big media budgets.

The biggest problem with happybrush is that they do not provide anything better than competitors. Amazon now offers regular delivery of selected items — amongst them head brushes — through Subscribe & Save and — as mentioned above — their products are neither cheaper nor better than existing offerings.

I am not saying that toothbrush incumbents cannot be beaten (just look at Amabrush, the toothbrush that automatically brushes your teeth in ten seconds, which has raised more then $3 Million on Kickstarter instead of the aimed $50.000), but to me happybrush is on the wrong path with their smart features and only slightly better products.

Notes

[1]

- PayPal statistics: https://www.paypal.com/de/webapps/mpp/pay-online

- paydirekt statistics: https://www.paydirekt.de/kaeufer/index.html, https://www.handelsdaten.de/handelsthemen/online-payment

PayDirekt actually reports to be available at 8000 (1500 independent online shops and more than 7000 shops on rakuten.com.). I disagree with this calculation because it does not change the amount of shops where paydirekt can be used.